TAX-EFFICIENT ASSET LOCATION

TAX-EFFICIENT ASSET LOCATION

Optimizing Investments to Minimize the Tax Bite in Retirement

DISCLAIMER: The information provided herein is on an as-is basis and only for informational purposes.

NOTE: The source for this article comes from the webinar on this topic given by Andy Panko of Tenon Financial and hosted by Tom Dickson on the Financial Experts Network.

INTRODUCTION

There are tax implications to virtually every aspect of a person’s financial life, especially in retirement. Things get complicated when considering portfolios of different investment account types and assets: regular brokerage accounts, tax-deferred accounts, Roth accounts, health savings accounts, social security, pensions, life insurance, home equity, all these things converge. And there are tax implications to all of it. The goal is for clients to live well in retirement, distribute from their portfolios as necessary, and do it all in a cohesive tax-efficient way. Achieving all this is the essential question of traditional asset allocation-- stocks versus bonds versus cash, etc. But it’s also the challenge of optimizing investments across different account types to have the least tax bite down the road. That’s asset location: what investments best go in which account type? Doing asset allocation efficiently can help ensure clients have the resources they need to enjoy the retirements they want for the duration of those retirements.

Keep in mind that although it’s critical to try to keep grounded in sound fundamental logic, there's no exact science to financial planning. These strategies should add value if done correctly, but there isn't a single right mix or “perfect” answer optimal for all clients. Many of the variables in this process are subjective and represent educated guesses about investment returns, tax legislation, life circumstances, etc. All these things change. So it's impossible today to pinpoint with laser precision what the best answer about asset allocation, location, and utilization will be for any given client. Only hindsight is 20/20. We have to do it the best we can with what we know, assume, and what tools we apply to the challenge. That's where all this fits in.

ASSET ALLOCATION: THE 60/40 RULE

Getting asset allocation wrong can have harmful impacts and derail someone's goals. If you need growth but let a client be conservative and park everything in cash, earning no interest, that’s a big problem. They may outlive their money. On the flip side, having too much risk can also be detrimental, especially for someone who needs most of their portfolio to spend down. You don't want that getting blown from risky investments gone bad. So proper asset allocation is critical.

To achieve a healthy, diversified portfolio, the traditional split of a client’s assets is 60% stocks and 40% bonds. This allocation can be done on an aggregate basis. Whether you have one account or 100 accounts on a rolled-up basis, this is your 60/40. How do you implement that across your different accounts? Let's assume you have a client with three accounts: a regular taxable brokerage account, a Roth account, and a tax-deferred account--a 401k, 403b, or IRA, etc.--you can invest in each of these different account types identically in that 60/40 portfolio. You can invest each of these different account types identically in that 60/40 portfolio. A lot of the larger places do precisely this. They run clients through a model, determine 60/40 is the right mix, and they'll simply take every account the client has and apply the same allocation.

That's one way to do, and again, as long as the allocation’s correct, that's the most important thing. But you can do better with the location of the assets.

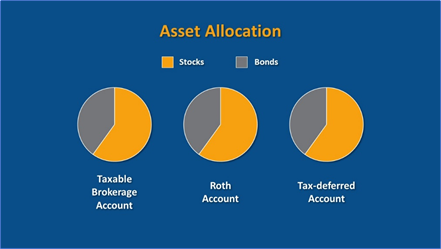

ASSET LOCATION

The overall goal continues to be at the 60/40 split between stocks and bonds on an aggregate basis. However, instead of uniformly applying this split across all account types, stack stocks and bonds differently to take advantage of each type of account’s tax implications and advantages.

So, for example, the taxable brokerage account, what if that's 80% stock, 20% bond? What if the Roth is 60/40 stocks to bonds? And the tax-deferred account is 20/80 stocks to bonds? (These splits are simply for illustration purposes only; every client’s situation will be unique.) You are now optimizing the ways different types of assets will likely perform over time in the individual tax structures of the account types. And even though the different account types might have allocations other than 60/40, in the aggregate, they sum up to 60/40, so the client’s overall asset allocation remains ideal.

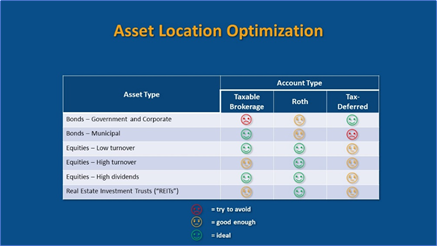

An in-depth discussion of what asset types are best suited for which account types is beyond the scope of this article, as are all the unique considerations associated with individual clients. That disclaimer noted, the following simplified chart is simply intended to illustrate in broad strokes some sense of what kinds of assets go well in which accounts and what doesn’t.

BONDS

The only assets to try to avoid putting in regular taxable brokerage accounts are government and corporate bonds. With these bonds, the total return is a function of the coupon interest they pay and the difference from the prices you buy them at to the prices at which you sell them. Any interest paid is taxable in the year received as ordinary income. So for government and corporate bond coupons sitting in regular brokerage accounts, all the interest will be fully taxed as ordinary income. These bonds are not bad options for Roth accounts--no asset type is “bad” in a Roth--but given the annual contribution limitations of retirement accounts, there are better options than bonds for Roths. So that leaves tax-deferred accounts as the best option for them. If located in a tax-deferred account, the interest on these bonds will accumulate tax-free, taking advantage of the magic of compounding until the client is ready to take a distribution.

Municipal bonds, on the other hand, are not suitable for tax-deferred accounts. The “big magic” of municipal bonds is (in almost all cases) they don’t get taxed at the federal level. However, if you put them in a tax-deferred account, the issue becomes any eventual distributions are all taxed as ordinary income, including the accumulated interest. You're taking a coupon that would have been tax-free had you had it in a regular brokerage account and subjecting it to full ordinary income tax rates. Not optimal.

EQUITIES

Assuming the client has met all the qualifying criteria, is over 59-and-a-half, the most tax-efficient environment for equities is a Roth account because all distributions will be tax-free.

Low-turnover equities are stocks or ETFs held for 12 months or longer and thus receive the more favorable (lower) long-term capital gains treatment on their appreciation in price. The qualified dividends of dividend-generating equities are also taxed at the more favorable long-term capital gains rates if the client holds the assets for longer than a year. Thus, low-turnover and longer-held high-dividend equities are well-suited for regular taxable accounts.

High-turnover equities, those sold within 12-months get taxed as ordinary income no matter what, so there is no particular disadvantage putting them in tax-deferred accounts.

Another consideration for tax-deferred accounts is you probably don’t want to have high-growth equities in them if you can avoid it. None of us know what tax rates will be in the future, but it is almost inevitable they will go up at some point. The argument to be made is if you can’t park these assets in a tax-free Roth, you will want to subject them to the most favorable tax treatment you can achieve now and not leave it to whatever the ordinary tax rate will be in the future.

CONCLUSION

Once again, the above discussion is for illustrative purposes only and is intended to encourage you to think about the subject. Every client’s situation, needs, and desires will be unique, as will be any solutions you develop. Overall asset allocation, the balance of equities and bonds in a portfolio, is the more critical retirement-planning function. Asset location, optimizing what assets go in which kinds of accounts, adds incremental value, especially for long-term tax-planning purposes. But any edge we can give to our clients will be appreciated by them.

Continue learning with our latest financial expert sessions

Explore upcoming webinars, gain industry insights, and stay ahead with expert-led education.

Explore Webinars